B1: BACKLOG

A backlog is simply a build-up of unfinished work. Backlogs can affect numerous business units within a business and can be a regular part of discussions in the finance, accounting and administration type roles. When it comes to project delivery, backlogs have the potential to delay phase completion and ultimately scheduled go live dates. The project manager needs to manage backlogs and analyse the route cause in order to help alleviate and eradicate any bottlenecks that are causing such backlogs.

The reasons for backlogs can be many but some include bad management, poor resourcing, lack of knowledge and experience, poor business processes, lack of investment, quality issues, testing and so on. Once backlogs become an issue the focus has to be on reducing theses down so that any delays in project delivery are eliminated. From an administration perspective backlog can be managed via RAID and action logs and also in house Information technology issue management systems such as Service now (SNOW) and Workday.

B2: BACKUP

With any file, folder or plan we save down to a network it is advisable that we back this up. A back up file can be saved in the cloud, simply saving it to an email account or using cloud services like Microsoft one drive or Dropbox. These services if used personally or through business can incur a monthly subscription. It all depends on the storage capacity you need or think you will need. When it comes to project plans and data it is advisable to always hold a backup. Security breaches including hacking, Trojan horses can render your work redundant and unretrievable. To safeguard against this companies do require employees to back up all materials saved locally. For personal accounts the same would be advisable.

B3: BAR CHART

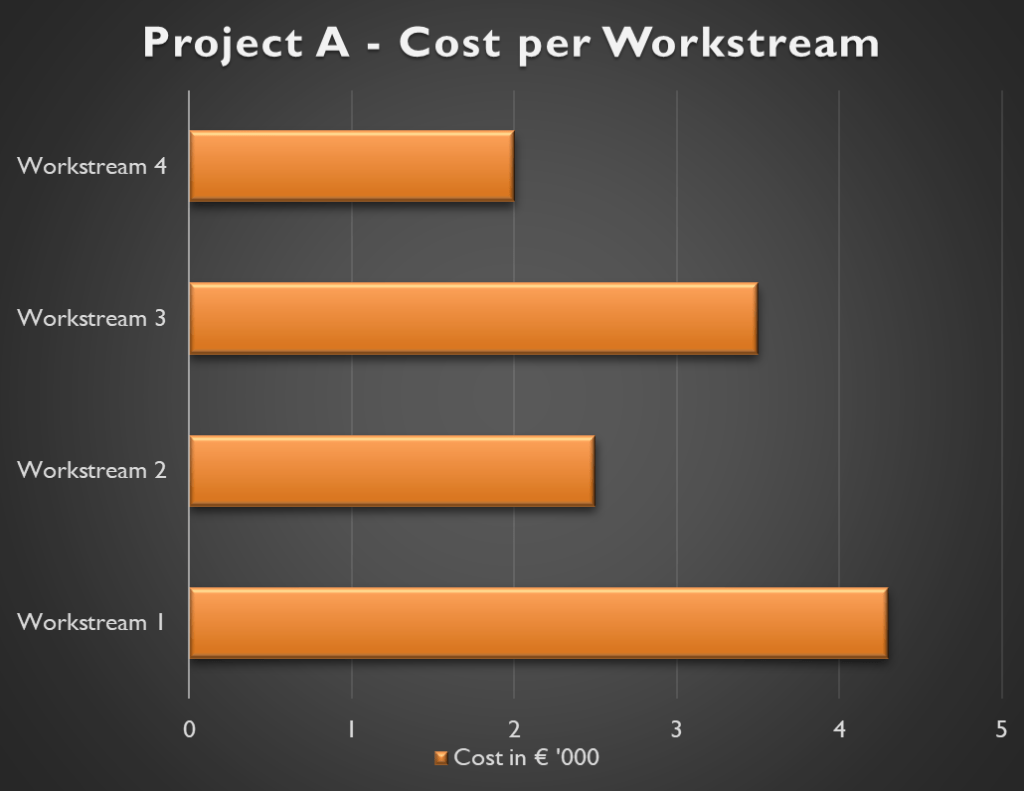

Bar charts are commonly use in financial analysis and can be an effective way of demonstrating project data for stakeholders. For example, a bar chart could display the percentage of a budget spend for each workstream or sub project as part of a program of project deliverables. The information is displayed using rectangular bars or columns. Key information and data can be displayed vertically or horizontally.

A simple example is included below depicting very simply costs incurred for project workstreams. Workstream titles are displayed on the Y-axis and cost in the X-axis. All bar charts can be jazzed up and various colours added to improve presentation and depict information in the format you deem fit.

B4: BASELINE PLAN

The one thing that is certain about planning is that you need to be prepared to replan and replan. But there has to come a stage where an agreed version of the plan becomes the baseline plan which is tracked against as the original plan. During traditional waterfall methodologies the baseline plan will be agreed after requirements are agreed and signed off either internally (if an inhouse project) or by the customer if an external project.

The baseline plan should use in the subsequent phases to track against and note delays in tasks and milestones. The plan can be updated and the baseline plan can be replanned and replanned if necessary but the new plans will be categorised as plan version 2, 3, 4 etc and these new plans will be tracked against the baseline plan to track variances and delays.

In the planning phase before a baseline plan is agreed, planning can take place and a project plan can be drafted but with the caveat and understanding that it is only a draft version until it is baselined.

B5: BEHAVIOUR

Behaviour of project team members is a key variant and constraint of project delivery. Behaviour deals with how individuals conduct and carry themselves towards others. This is of critical importance because with any project you will deal with a magnitude of different personalities, some passive, some passive aggressive and some aggressive and belligerent. It is the job of the project manager to manage all stakeholders including their personalities.

Offensive and bullying behaviour is not to be tolerated but some stakeholders will have an aggressive demeanour about them and may not be the most pleasant to work with. Astute management and control of such behaviours by the project manager will help aid the primary goal of getting a project completed in time, within scope and budget.

With experience comes the ability to manage difficult situations and not to take issues personally. Conflict and difference in working style between project team members has to be facilitated but not to the detriment of the project. If stakeholder’s behaviour becomes a liability and hurtful to other team members then these behaviours need to be reported and escalated to senior management and possibly human resources. Previous experience in managing large and complex projects will aid the project manager in finding the correct balance here.

B6: BENCHMARK

A benchmark is a target or reference point that a thing or project can be compared against. You may be comparing targets for delivery against competitors or against different internal business units. A PMO (Project Management Office) may dictate that the benchmark for project completion is 6, 9 or 12 months, depending on the system, product, process or service being delivered. What benchmarks strive to achieve is a way of monitoring and managing targets. If no benchmarks existed for example within project delivery, then delivery could become adhoc and too flexible. Flexibility as part of agile project delivery is welcome but it has to be managed and benchmarked accordingly.

B7: BENEFITS ANALYSIS (CBA)

Benefits analysis (known also as a cost-benefit analysis CBA) is a common process used in business to determine if a particular decision is worth undertaking or not. It could be for example a decision on whether a project is worth pursuing or not. It should contain an analysis on the tangle rewards and costs involved, anything that can be measured financially and whether the reward outweighs the costs. Intangible items such as customer satisfaction, reputation etc can be analysed too but these can only be estimated.

Some outputs of CBA should be

• A measure of the benefits / reward of pursuing a decision minus the costs associated with implementing it.

• Financial metrics should be used to ascertain the results needed.

• Should include intangible benefits such as customer satisfaction, useability etc as mentioned above.

• Complex analysis can be undertaken to include *sensitivity analysis, *discount rates, *net present value (NPV) calculations, what if *scenario analysis etc.

• Information that can form the basis for a favourable or unfavourable decision on whether a project can be undertaken or not.

*These items will be discussed in more detail in future posts.

So why should companies undertake CBA? Well for manager to understand the financial implications of undertaking a project or not CBA should provide enough information to make such a decision and confirm whether the project is financially feasible or not. It should also factor in the opportunity costs involved which are costs foregone because of choosing one path instead of another. For every decision we make even in basic day to day life decisions there is a missed opportunity or cost of doing this as a result of the choice / decision we make. The same exists in business.

When opportunity costs are included, the CBA is more accurate and complete and gives managers a wider depth of information in order to make their final project decisions. When all the costs are known and considered they should be compared quantitatively to see if the rewards outweigh the costs. If the rewards are more than the rational decision should be proceeded with the project, if the opposite then rejecting the project becomes the rational decision. However not all decisions will be as simple as that and if the reward only outweighs the costs by negligible amounts, then rejection is probably likely. If any of the financial forecasts or models built into the CBA process contain inaccurate assumptions or information than the result cannot be trusted and this is a risk of CBA.

There are steps to follow when executing a CBA and they are not set in stone. An example of a process to follow is below

1. Identify the scope of the project – at this stage you should identify the what you are proposing to implement, whether this is a new system or what business metric you are trying to change, this could be an expansion of your business to new markets. The full scope needs to be assessed and understood. The implications of the scope need to be known, for example, increase in technology, increase in resources, impact on current day to day business etc. All key stakeholders need to be made aware of the proposed project and allowed time to digest it and give feedback.

2. Cost the project – once part one is completed and the scope is understood, then the cost of the project will need to be estimated and determined based on the current information at hand. What needs to be included is:

a. Direct costs which would be labour, materials, stocks and any other expenses incurred relating to these areas

b. Indirect costs which are overheads such as electricity, rent and all utilities used.

c. Intangible costs which are the costs you can not see such as employee / customer satisfaction, business reputation, timelines etc

d. Opportunity costs which as mentioned are the cost foregone because of choosing one option over another, for example choosing System A instead of System B.

e. Managing risk such as regulatory and compliance risks, impact on direct competition, environmental, economic and political risks. The risks incurred are dependent on the nature of the business you are in but a lot will crossover such as legal and regulatory risks.

3. Ascertain the benefits – the benefits derived from any decision or / and project are unique to a particular business. Some of the benefits can include but are not limited to the following:

a. Increased productivity

b. Technology improvements

c. Enhance customer / staff satisfaction

d. Enhanced business reputation

e. Increased market share either domestic / international

f. Streamlined service offering

g. Increased sales and profitability

h. Increased competitor advantage

A project manager or cost analyst should attach a monetary cost to all benefits. The cost should be the best estimate known factoring in all the knowledge attained at the time, and special attention needs to be taken to make sure no under or overestimation of costs is included.

Two further areas to consider when calculating costs are implicit and explicit benefits. These are pretty much the same as intangible and tangible benefits. With explicit benefits the risk is that the wrong assumptions could be made regarding future market conditions even in the short term. Assumptions will have to made about projected sales and customer demand. Also, market conditions need to be factored in and if any known political or economic event is coming then these need to be included. For implicit benefits assumptions and estimates are harder to gauge and calculate and can remain unknown until the product or service is delivered. For example, employee morale and satisfaction and how they cope with change will only be known when the project is delivered and live. When all the above is factored in measuring benefits is not an exact science but more often than not a best estimation.

4. Analyse the calculations – At this stage you should have the data, specifically figures that will determine whether a project is viable in monetary terms. If the outcome is that the benefits are higher than the costs than the decision should be to proceed. However, it may not be as simple as that. Other low-level techniques can be used to determine more accurate costing.

a. Apply discount rates to ascertain what the net present value of cashflows is.

b. You can use different discount rates depending on the project situation.

c. Potentially calculate a CBA for different options, if you have the data. Each option can have different costs and benefits.

d. Calculate costs benefit ratio for each option

e. Perform sensitivity analysis on the options which should show how small deviations in costs / benefits will affect the outcomes.

5. Make recommendations on accepting or rejecting the project – Now you have the calculations and the analysis, so it is important the information is presented concisely and clearly to management in order for them to make the correct decision.

If the benefits are greater than the costs that logic will dictate a positive project outcome. However, management can have information that operational staff are not privy too such as increased market cost, future events, potential redundancies or/and resource constraints, project risk, limited availability of capital and so on. Therefore, positive results may be rejected based an overall effect on the business and not just because potential benefits outweigh costs.

Advantages (Pros) of Cost-Benefit-Analysis (CBA)

▪ Data drives analysis and results.

▪ Focused analysis used to determine if projects are viable in quantifiable format.

▪ Aids strategic planning for senior management.

▪ Measures financial and no financial data i.e. customer satisfaction, company reputation.

▪ Can be useful for small and medium sized projects to make informed and rational project decisions.

▪ Findings of CBA should provide reliable and accurate data.

▪ Techniques like net present value provide data that determines returns that could be earned elsewhere, which shows the minimum a project needs to earn to be deemed viable.

Disadvantages (Cons) of Cost-Benefit-Analysis (CBA)

▪ For large projects it can fail to take account of economic conditions and financial concerns such as inflation, interest rates, cashflows volatility and the present value of money.

▪ Not useful for small and medium projects as findings are limited in their business value.

▪ Bases a lot of findings off forecasted models and estimated figures and the risk with this is that the assumptions prevailing at one particular moment in time may be inaccurate or simply could change in the future.

▪ Can be resource and capital intensive.

Reference: What Is Cost-Benefit Analysis, How Is it Used, What Are its Pros and Cons? (investopedia.com) by Adam Hayes